Financial advisory

Financial advisory for the critical moments that define your business’ success, with Mazars' expertise in deals, financing and crisis & disputes

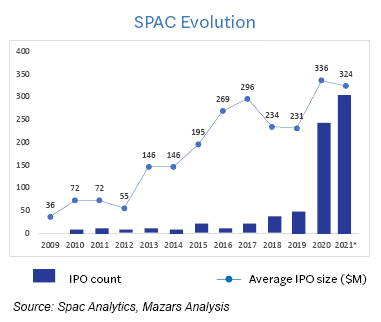

The issues associated with the traditional IPO listing and the burden of regulatory paperwork have diverted attention to SPACs which boast a quick and efficient route to go public.

Historically, investors and founders were sceptical of SPACs due to their poor financial performance. However, with excess capital in hand, the tide has turned, and SPACs are becoming an important component of the capital markets landscape.

In recent years, many well-known investors including hedge funds and private equity fund managers have joined the SPAC race. They have brought expertise and credibility to SPAC, cementing its position, not just as the hottest investment vehicle, but also a reputable one.

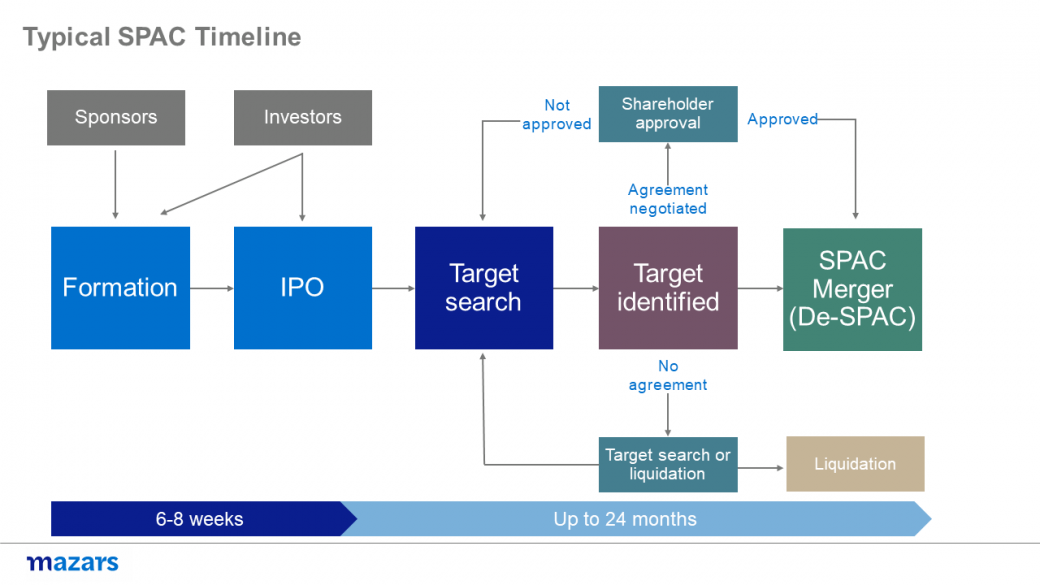

Typically, a SPAC has a two-year window to search and acquire a target company. After a target company is identified, shareholders vote and choose to either merge with the target company, search for new target company, or liquidate the SPAC.

Once shareholder approval for target company is received, the SPAC merges with the target company, this process is called De-SPACing.

A SPAC formation involves an experienced management team or sponsor who pays a nominal amount for generally, a 20% ownership of the SPAC share stake. This is often known as the founders’ shares, which reward the initial investors for funding the capital and identifying a promising target.

The sponsor may also be expected to loan additional funds if the SPAC requires additional capital to pursue the business combination or pay other expenses.

After formation, the SPAC then raises capital by issuing units for the remaining 80% interest through a public offering. Each unit consists of a common share and a fraction of a warrant.

Founder stocks and public shares generally have similar voting rights with few exceptions, namely only sponsors with founder stocks can select the SPAC directors. Institutional investors and warrant holders typically do not have the same voting rights as only whole warrants are exercisable.

At least 90% of the IPO proceeds are held in a trust or escrow account until a target company is acquired. The account must be opened with and operated by an independent escrow agent which is part of a financial institution licensed and approved by the Monetary Authority of Singapore. The funds can be released for the redemption of public shares if the SPAC is unable to complete a business combination.

Under the Singapore Exchange (SGX) framework announced on 2 September 2021, a SPAC in Singapore has 24 months to identify and complete a de-SPAC transaction. An extension of 12 months may be considered under prescribed conditions.

Similar to any M&A transaction, the SPAC must undertake the necessary due diligence to assess a target company and its value. Then, it must issue a circular to shareholders to inform them of the potential business combination as well as a valuation report which includes audited historical financial statements.

Following the identification of the target company, the SPAC will undertake a mandatory shareholder vote. The SPAC needs to provide sufficient time to ensure an active solicitation period and an informed shareholder vote.

The business combination must be respectively approved by a simple majority of directors and by a resolution passed by shareholders.

When the conditions in the agreement are satisfied, the merger will be consummated in the De-SPAC transaction. Subsequently, the SPAC and the target business will combine into a publicly traded operating company.

The sponsor’s founders’ shares and warrants will be under a lock-up period for one year after the closing of the De-SPAC transaction, but it is subject to an early termination. The SPAC would also be subject to continuing listing obligations under the SGX listing manual.

Below are the requirements that need to be met prior to a De-SPAC completion:

How we can help

With the inclusion of seasoned auditors, IFRS experts, capital market, tax and transaction specialists, Mazars in Singapore provide exceptional services and deep insights on SPACs. We offer the following services:

Financial advisory for the critical moments that define your business’ success, with Mazars' expertise in deals, financing and crisis & disputes

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.