Transfer pricing

A global view on a business-critical, fast-evolving issue

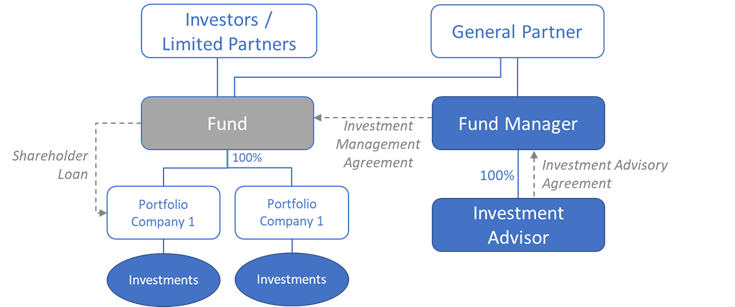

Fund management is a regulated activity in Singapore. Investment funds in Singapore are commonly managed by fund managers or investment advisers which hold a Capital Markets Services licence or are exempted from it. A typical fund structure is as follows:

In this case, as the fund manager and the investment advisor are related to the General Partner, which holds an interest in the fund (by way of shareholding or control), the transactions between these entities are considered as related party transactions from the tax perspective.

Recent developments in BEPS and potential impact of more aggressive transfer pricing audits show the increasing importance of ensuring that all related party transactions are consistent with the arm’s length principle. Additionally, if the annual gross turnover of a Singapore entity exceeds the threshold of SG$10 million, there is a requirement to prepare Singapore transfer pricing documentation.

Some of the common related party transactions in the asset management space include:

Frequently Fund Managers delegate part of its asset management activities to other group entities and may manage multiple funds within the group set up to hold different types of underlying investments. Accordingly, the remuneration of the Fund Managers should take into consideration their functions, assets and risks and their contribution to the overall value creation process. Below are the typical transfer pricing methods used to determine the arm’s length transfer pricing for intragroup services in the asset management sector:

The transfer pricing for asset management activities is a complex issue that needs to be carefully considered. With our team of experts in the financial service sector, we can help you identify the potential transfer pricing risks arising from your fund management activities and provide the right solutions for your specific needs.

A global view on a business-critical, fast-evolving issue

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.