Tax

Insight and innovation to guide you through today’s evolving global tax landscape

Model Rules published in 2021 set complex mechanisms of how to compute the groups’ effective tax rates (ETR) and any top-up to be collected. A new reporting regime which requires substantial new forms of financial data to be reported to the ultimate parent company locations which implement Pillar 2 is also announced. These standardized GloBE Information Returns will need to be submitted annually in addition to country tax returns.

Essentially, Pillar 2 requires the ultimate parent entity (UPE) to pay a top-up tax on its proportionate share of the income of any low-taxed subsidiary and permanent establishment (unless specifically excluded) in which the UPE has a direct or indirect ownership interest to bring the overall tax on the profits up to the 15% ETR.

More than 130 countries have signed up to the OECD inclusive framework and a number of countries in EU, UK and Asia have issued draft legislations to implement Pillar 2 as early as 2024 with the first GloBE Information Returns due to be filed by June 2026 for financial years ending 31 December 2024.

It remains to be seen whether countries implementing Pillar 2 will follow the design of the Model Rules closely and if otherwise will add further complexity. The different implementation timelines of the countries can also result in further complexities on how the top-up tax may be calculated.

Singapore will similarly implement Pillar 2 on or after 1 January 2025. This will no doubt have a significant impact on Singapore companies currently enjoying tax incentives on qualifying income to be taxed between 0 to 13.5%.

The ETR and top-up tax calculations are very complex and require a large amount of data which is not currently collected by most MNE groups. Any group operating in multiple jurisdictions or with a large number of entities will suffer a significant data collection and manipulation compliance burden. All MNEs which will be caught by Pillar 2 should start to assess the impact of these Rules and plan how to configure existing systems/processes to capture these new data points, put in place processes and resources to prepare the GloBE Information Returns, etc.

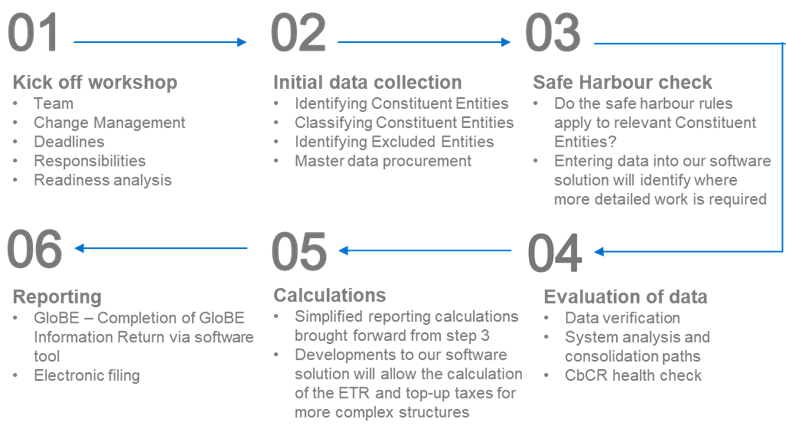

Mazars have the knowledge, expertise and capability to assist you in the Pillar 2 preparation. We will tailor the approach below to fit each client.

Insight and innovation to guide you through today’s evolving global tax landscape

Singapore is looking to update its corporate tax system to account for global tax developments relating to BEPS 2.0.

Rapid digitalisation and globalisation have led to significant changes in business operations. The digital economy has also uncovered vulnerabilities in the basic rules that have governed global taxation in the past, creating opportunities for profits to be “shifted” to lower taxed jurisdictions and sparking debates surrounding a 'fair’ allocation of taxing rights.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.