SPACs in Singapore

The Special Purpose Acquisition Company or SPAC trend has surged in popularity in recent years. Generally known as a US market innovation, this investment vehicle is prompting a seismic shift across global financial markets.

A SPAC is a shell company formed to raise money from investors through an IPO. The SPAC is then used to acquire private companies, known as target companies, without having to go through a formal IPO process.

At the time of the IPO, SPACs typically don’t have existing business operations or specified targets. That’s why they are often called blank cheque companies. The SPAC is formed for the purpose of identifying and acquiring businesses that meet the SPAC’s investment objectives. The private target company effectively becomes a publicly traded company, generally via a merger transaction or acquisition of shares (called business combination).

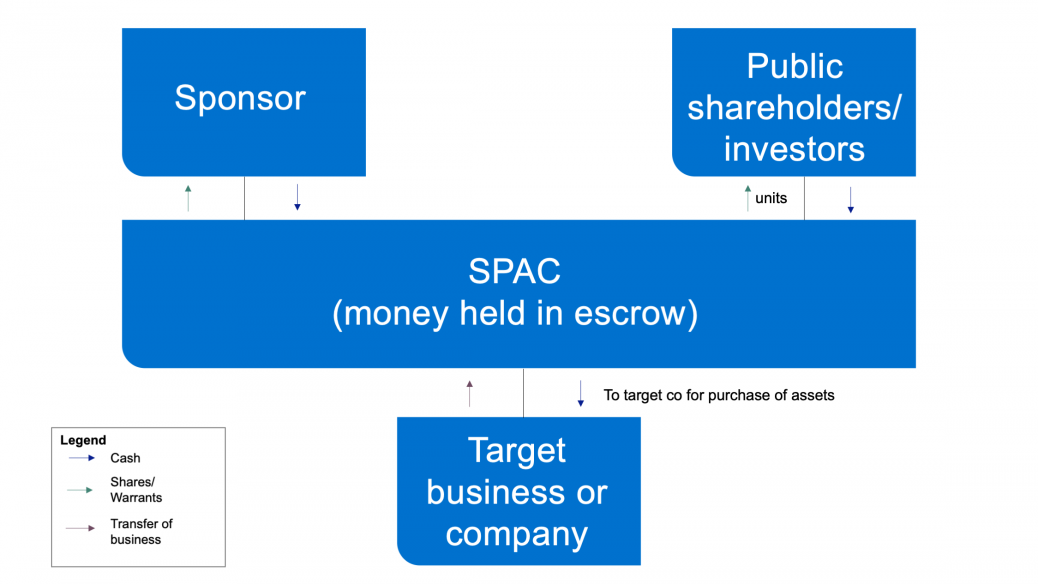

This could be a typical structure:

Key tax issues

Businesses need to carefully consider the tax issues arising from SPAC transactions to fully reap the benefits of this investment vehicle.

The tax considerations include:

SPACs are set to emerge as a powerful force in the Singapore capital market. Understanding the key tax issues and receiving the proper tax advice is paramount to success.

Mazars can help you structure the SPAC and de-SPAC tax efficiently. We have experience in structuring and leading multi country M&A projects for many years.

In addition to tax due diligence/structuring support for listing SPACs, other areas of support that Mazars can offer are valuation, financial due diligence, M&A advisory, setting up of new entities, and compliance support.

Our experts are here to support you through the SPAC process, providing tailored solutions and expert advice to help you focus on the big picture and make the key decisions throughout the process.

The Special Purpose Acquisition Company or SPAC trend has surged in popularity in recent years. Generally known as a US market innovation, this investment vehicle is prompting a seismic shift across global financial markets.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.