Transfer pricing

A global view on a business-critical, fast-evolving issue

Based on the statistics provided by the Singapore Economic Development Board1, there are 1,100 family offices established in Singapore as of 2022.

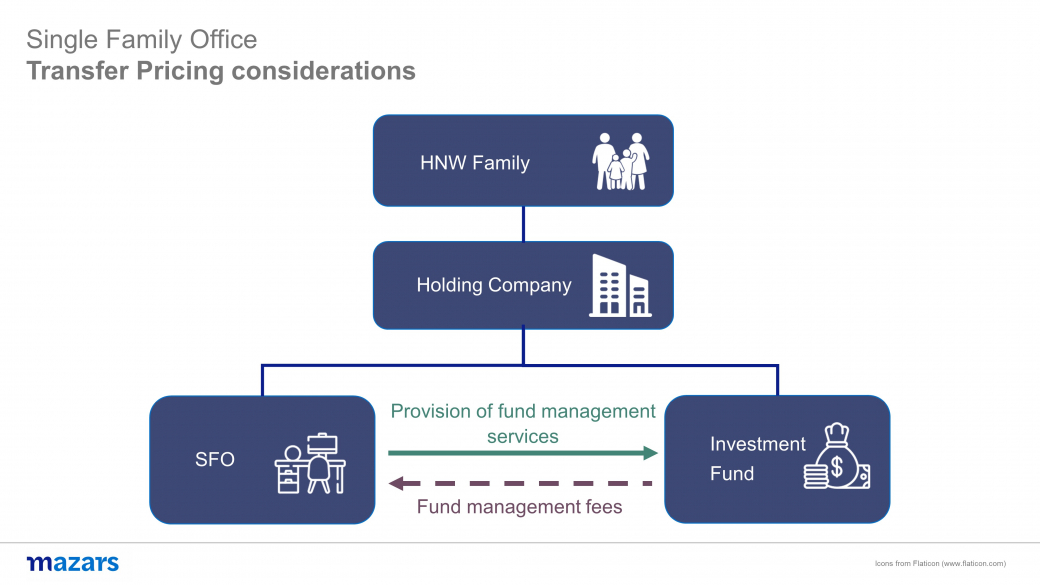

We will focus on the transfer pricing considerations for SFOs which manage assets for and on behalf of a high net worth (“HNW”) family:

If the SFO and Investment Fund (i.e., the fund entity) are controlled by the HNW Family, services provided by the SFO to the Investment Fund would be considered as related party transactions which must comply with the arm’s length principle under the Singapore Income Tax Act.

The commonly seen pricing policies adopted for the related party services transactions such as discretionary investment management and support/administration services could be a percentage on investment profits or fund size or mark up on cost base. However, these will not preclude the Inland Revenue Authority of Singapore (“IRAS”) from challenging the reasonableness of the pricing policies adopted and the comparability analyses conducted.

It is crucial for the taxpayer to maintain a certain level of documentation and analysis to substantiate the relevant pricing policy adopted. If IRAS is not satisfied that the related party transactions were conducted on an arm’s length basis, transfer pricing adjustments may be made. Once a transfer pricing adjustment is made by IRAS, this adjustment is subject to 5% surcharge regardless of whether there is tax payable on the adjustment. The surcharge is not deductible for tax purposes.

At Mazars, we have the expertise in advising the following:

If you have any questions, please don’t hesitate to get in touch with our Tax Experts.

Do you have any questions for us?

__________________________________________________________________________________

1 https://www.edb.gov.sg/en/our-industries/family-office.html

A global view on a business-critical, fast-evolving issue

Insight and innovation to guide you through today’s evolving global tax landscape

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.